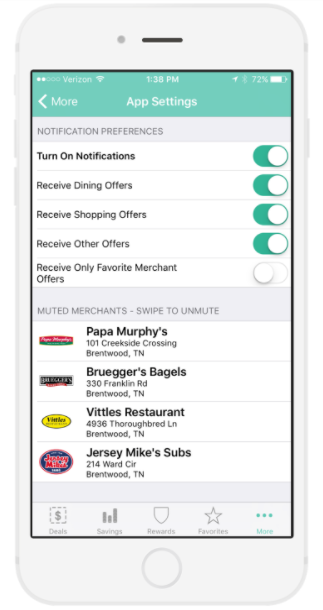

With the CBC Perks+ mobile app, customers can be notified when they’re near your store

Location aware discounts in the CBC Perks+ mobile app mean customers can get app push notifications to remind them they’re near your store. Joining...

2 min read

On May 24, 2018, President Trump signed the Economic Growth, Regulatory Relief and Consumer Protection Act into law. The Independent Community Bankers of America (ICBA) advocated for its passage, saying that this would help Main Street communities across the nation by assisting with consumer access to business and credit lending. With this law, there will be changes to banks that should help communities grow economically. It will benefit banks of all sizes, and will be especially helpful to smaller community banks. You can read the full text and analysis of the new regulations by the American Bankers Association here.

On May 24, 2018, President Trump signed the Economic Growth, Regulatory Relief and Consumer Protection Act into law. The Independent Community Bankers of America (ICBA) advocated for its passage, saying that this would help Main Street communities across the nation by assisting with consumer access to business and credit lending. With this law, there will be changes to banks that should help communities grow economically. It will benefit banks of all sizes, and will be especially helpful to smaller community banks. You can read the full text and analysis of the new regulations by the American Bankers Association here.

Benefits for Large Banks

Banks with $250 billion or more in assets gain more relaxed capital requirements and changes to the Volcker Rule. Large regional banks that have between $50 billion to $250 billion in assets can also receive some benefits by being exempted from the Comprehensive Capital Analysis and Review (CCAR). The number of banks that now have to take that test dropped from 38 to 12. However, banks with over $100 billion in assets will have to take the test one last time before becoming exempt.

Benefits for Small Regional Banks

Smaller banks between the $25 billion and $50 billion asset range have lots to gain from this new law. They are immediately exempt from the CCAR and don’t face as much stress with regulatory costs and capital costs. Before, passing the $50 billion threshold would have been intimidating for smaller banks, but now they can focus on working toward growth.

Benefits for Community Banks

Smaller banks beneath the $25 billion threshold, also known as community banks, may be the real winners because of lower regulatory costs and a simplified capital regime. Banks with assets less than $10 billion will see a more simplified capital regime because of a community bank leverage ratio between 8 to 10 percent for tangible equity and average assets.

If banks have less than $10 billion in assets, they are exempt from the Volcker Rule, which limits hedge fund and equity fund investments and doesn’t allow commercial banks to engage in proprietary trading. Before, community banks complained about this rule because it indirectly targeted them. Even though it wasn’t meant to affect them, it still created another regulatory burden because they had to prove their compliance with the rule.

It will also be easier to receive qualified mortgage status, which was an obstacle in the past. Additionally, the exam period will extend from 12 months to 18 months if a bank has less than $3 billion in assets. Previously this was only available to banks with less than $1 billion in assets.

John Medina, First Federal Senior Executive Vice President, had this to say about the new law.

“The S. 2155 Act that was recently signed into law provides relief from several regulatory requirements for both consumers and community banks. On the consumer side, the act will lift a few of the restrictions for getting a mortgage and includes protections for veterans and consumer credit. On the community bank side, several provisions will allow us to be more flexible with investments, better understand cybersecurity threats, and make it easier for customers to do business with us. A couple other provisions will permit us to submit less paperwork, which will allow us more time to focus our efforts on serving our customers.”

Location aware discounts in the CBC Perks+ mobile app mean customers can get app push notifications to remind them they’re near your store. Joining...

To a novice borrower, the SBA lending world can oftentimes be quite confusing, and borrowing can seem a daunting task. But, with the right SBA...

For more than 50 years, National Small Business Week has honored small businesses and their contributions in the United States. More than half of...